April 13, 2012 01:07 PM | Permalink |

Read the PDF of this report.

Tax Planning for the Super Wealthy

Millions of Americans will spend part of this upcoming weekend trying to navigate tax preparation software or filling out the actual paper forms to file their income tax returns before the Tuesday deadline. For those wishing they could pay less tax, outlined below are some tax planning ideas taken from a review of presidential candidate Mitt Romney’s tax returns.

Don’t Work for a Living

The single best way to reduce your income tax bill is to make sure that your income is subject to the lower preferential rates for dividends and capital gains. The federal tax system taxes “ordinary” income, like salaries and wages, at much higher rates (up to 35%) than investment income (maximum 15%). Many states have capital gains tax breaks, too. The low capital gains tax rate explains Romney’s 14 percent effective federal income tax rate. Almost all of his income is taxed at the low rate — the ordinary income he does have, from interest and speaking fees, is mostly offset by his itemized deductions.

At any level of income, a taxpayer with income from capital gains and dividends will pay less than half of the federal income tax paid by a taxpayer with the same amount of wages. Here are some examples:

|

Federal Income Tax

|

If Wages

|

If Capital Gains

|

|

Single, doesn’t itemize, $60,000 income

|

$8,750

|

$2,400

|

|

Married, itemizes, $250,000 income

|

$43,400

|

$19,300

|

|

Married, itemizes, $20 million income

|

$6,276,000

|

$2,695,200

|

The wage earner pays payroll taxes on top of the income tax. So it’s best, like Romney, to be unemployed.

|

Federal Income and Payroll Taxes

|

If Wages

|

If Capital Gains

|

|

Single, doesn’t itemize, $60,000 income

|

$17,930

|

$2,400

|

|

Married, itemizes, $250,000 income

|

$63,900

|

$19,300

|

|

Married, itemizes, $20 million income

|

$6,867,100

|

$2,695,20

|

If You Do Work, Disguise Your Compensation as Capital Gains

Romney’s return does report quite a bit of compensation (in addition to that “not very much” in speaking fees of $529,000), but it’s disguised as capital gains, to make it subject to that special low rate. About half of the $15 million in capital gain and dividend income reported on his 2010 tax return is compensation from Romney’s partnership interests in Bain Capital funds.

These “carried interests” were earned by Romney in exchange for the services he performed while at Bain Capital. Private equity, hedge fund, and other investment fund managers structure their compensation so that most of it is received in the form of a partnership interest — a piece of the deal — and the income from those carried interests is taxed at the capital gain rate. In addition to paying a much lower income tax rate, Romney also avoids paying the Medicare payroll tax on the income.

Give to Charity — But Not Cash

If you give a gift of appreciated property, like stock, to a charity, your deduction is the value of the stock, even though you may have paid far less for it. In Romney’s return, there’s a deduction for just under $1.5 million worth of Domino’s Pizza stock (which he likely received in a Bain Capital deal) to the Tyler Foundation (more about that below). The price he paid for the stock was zero or something so close to zero that the accountant didn’t bother reporting it. Giving the stock to the foundation saved Romney an estimated $220,000 in taxes that he would have owed if he had sold the stock and given cash instead.

Give to Charity — But Not Now

In Romney’s tax return, there’s income from the W. Mitt Romney 1996 CRUT (that’s a Charitable Remainder UniTrust). That means Romney set up a charitable trust in 1996 (with a half million dollars or more) and he kept the right to receive income from the trust for a certain number of years or, quite likely, for the rest of his life.

In 1996 Romney got an income tax deduction for what will go to charity when the trust ends. The charity won’t get a dime until that trust ends (and it’s already been 15 years since the contribution), but Romney got a big deduction on his 1996 return (it’s hard to know how big without seeing the return). In addition, he or one of his close advisors can be the trustee of the trust and control the money until the trust ends.

In addition, the trust is a tax-exempt entity, so it can sell whatever assets are in the trust and pay no capital gains taxes, diversify Romney’s portfolio, and increase his investment return. Of course, at the end of the trust’s term, whatever remains in the trust must be distributed to a charity. In the meantime, Romney has enjoyed some generous tax benefits.

Give to Charity — Your Own

Of the almost $3 million in charitable contributions on Romney’s 2010 tax return, about half went to The Tyler Charitable Foundation which Mitt and Ann Romney set up in 1999. When Romney makes a contribution to the foundation, it is fully deductible on his personal income tax return that year.

The foundation itself doesn’t provide direct services like a soup kitchen does. The “private” foundation (whose donations come from only one or a few supporters) gives money to charities like the Boys and Girls Club (known as “public” charities because their support is from the public more broadly) that generally do provide direct services.

The foundation only has to distribute 5 percent of its assets each year. So while Romney got a $1.5 deduction for the amounts transferred to the foundation in 2010, the foundation can take its sweet time getting the money in the hands of a public charity. At the end of 2010, the foundation had over $10 million in assets.

Use Offshore Investment Vehicles

An American citizen is taxable on all of his income, no matter where he lives or where the income is earned. If the income is subject to any foreign tax, the taxpayer gets a credit against his U.S. tax, to avoid double taxation. Romney reduced his U.S. tax bill by almost $130,000 in foreign tax credits on his 2010 return.

The earnings on any foreign investments would be fully taxable in the year earned, so it seems there would be no tax advantage to investing offshore. But using certain foreign investment vehicles allows a U.S. taxpayer to avoid some rules and thereby save some tax.

(For tax nerds: Investing in a Bain Capital fund formed in the Cayman Islands through a PFIC (Passive Foreign Investment Corporation), for example, can save an individual investor tax by avoiding the limitations on miscellaneous itemized deductions. A tax-exempt investor, like Romney’s Individual Retirement Account, can avoid the Unrelated Business Income Tax (UBIT) by investing through a foreign corporation as well, instead of investing in the fund directly.)

There are reports that Romney may have taken advantage of the tax savings offered by investing through these offshore vehicles, although it’s not apparent from the tax return. The return does have 55 pages of forms for reporting Romney’s transactions with foreign corporations, foreign partnerships, and PFICs. At least eleven of the entities from which Romney earns income are located in countries considered to be offshore tax havens, such as Bermuda, the Cayman Islands, and Luxembourg.

Invest in Sexier Financial Instruments

If you’re investing in plain vanilla stock and bonds, you’re missing some tax planning opportunities. For example, Romney’s return includes a $415,000 gain from certain investments that get special treatment under the tax rules (for tax nerds: section 1256 contracts).

The gain on these investments is treated as 60 percent long-term capital gain and 40 percent short-term gain, no matter how long you’ve actually held the investment — even if it’s for only one day! The amount treated as long-term gain gets taxed at that special low capital gains rate. Romney’s return also discloses income from foreign currency transactions, swaps and other derivatives, and investments which are written up to market value each year.

Borrow Money Only to Invest

If you borrow money to buy a car, the interest is not deductible even if you need your car to get to work. If you use a credit card to buy personal items, that interest is not deductible. If you borrow money to buy a house, the interest is deductible but only on a loan of $1 million or less. (Romney’s three homes are valued in the neighborhood of $25 million.) If you borrow money against the equity in your home, interest on only $100,000 of principal is deductible.

But if, like Romney, your interest expense is “investment interest expense,” it is deductible, limited only by the amount of your investment income. When your investment income is in the millions of dollars, you can deduct a lot of interest.

Be Aggressive in Your Tax Planning

When a taxpayer engages in a type of transaction that the Internal Revenue Service has identified as potentially abusive, he must disclose that in his tax return. It’s called a “reportable transaction” and the taxpayer has to file a Form 8886 to tell the IRS about it. Romney’s 2010 return included six Forms 8886 (16 pages) related to investments in hedge funds and private equity funds.

But Don’t Do Anything Illegal

There’s nothing in Romney’s tax return that indicates anything necessarily illegal or improper. On the contrary, it appears that he has been conscientious in filing the necessary forms and disclosures.

In addition to the disclosures noted above, on Schedule B, Interest and Dividends, the “yes” box is marked on that pesky question about foreign financial accounts and “Switzerland” is shown as where the account is located. If Romney was going to use offshore accounts to illegally evade taxes (as opposed to merely avoid them), he might decide not to complete that part of the return or he might omit some of those disclosure forms.

For Your Return

While in theory any taxpayer could use the tax planning techniques outlined above, in reality only the wealthy can take advantage of them. It takes a substantial amount of money to set up a charitable trust, for example. In addition to the money you put in the trust, you have to pay the attorney who draws up the trust documents and the accountant who files the trust’s annual tax returns. So unless you’re making a pretty substantial contribution, the costs would outweigh the tax benefits.

You have to have significant resources to be able to structure your debt for the best tax result. Or to set up a private foundation. Or make offshore investments. Or structure your compensation as capital gains.

The fact that there doesn’t appear to be anything improper in Romney’s tax return — and yet the return is full of ways only a wealthy person can reduce his tax bill — is the problem.

The most straightforward way to implement the Buffett Rule would be to eliminate the personal income tax preferences for investment income. This would mean, first, allowing the parts of the Bush tax cuts that expanded those preferences to expire. Second, Congress would repeal the remaining preference for capital gains income, which would raise $533 billion over a decade.

The most straightforward way to implement the Buffett Rule would be to eliminate the personal income tax preferences for investment income. This would mean, first, allowing the parts of the Bush tax cuts that expanded those preferences to expire. Second, Congress would repeal the remaining preference for capital gains income, which would raise $533 billion over a decade. Senator Sheldon Whitehouse of Rhode Island has introduced a bill that would take a more roundabout approach to implementing the Buffett Rule by imposing a minimum tax equal to 30 percent of income on millionaires. This would raise much less revenue than simply ending the break for capital gains, for several reasons.

Senator Sheldon Whitehouse of Rhode Island has introduced a bill that would take a more roundabout approach to implementing the Buffett Rule by imposing a minimum tax equal to 30 percent of income on millionaires. This would raise much less revenue than simply ending the break for capital gains, for several reasons.

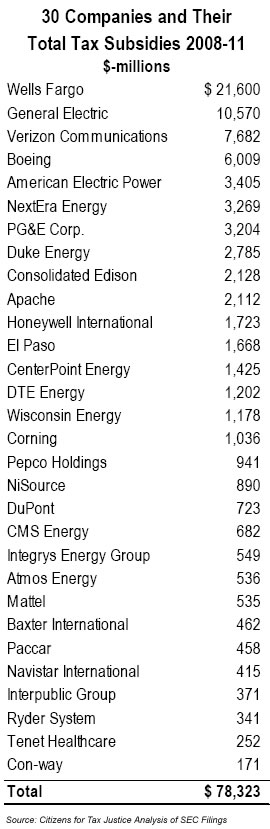

Had these 30 companies paid the full 35 percent corporate tax rate over the 2008-11 period, they would have paid $78.3 billion more in federal income taxes. Or put another way, over the four years, the 30 companies received more than $78 billion in total tax subsidies. Wells Fargo alone garnered $21.6 billion in tax subsidies over the four years, followed by General Electric ($10.6 billion), Verizon ($7.7 billion), and Boeing ($6.0 billion).

Had these 30 companies paid the full 35 percent corporate tax rate over the 2008-11 period, they would have paid $78.3 billion more in federal income taxes. Or put another way, over the four years, the 30 companies received more than $78 billion in total tax subsidies. Wells Fargo alone garnered $21.6 billion in tax subsidies over the four years, followed by General Electric ($10.6 billion), Verizon ($7.7 billion), and Boeing ($6.0 billion).

Unfortunately, most proposals to close corporate tax loopholes (including President Obama’s) would give all the resulting revenue savings back to corporations in the form of new breaks.

Unfortunately, most proposals to close corporate tax loopholes (including President Obama’s) would give all the resulting revenue savings back to corporations in the form of new breaks.