Shell games have been with us since ancient times, and the tax shift proposals of today indicate that the basic concept has a long shelf life. A “conjurer” who makes fantastic claims that are later found too good to be true? Kansas Gov. Sam Brownback and many other governors fit the bill. A “shill” who enthusiastically vouches for the legitimacy of the game and who stands to make a hidden profit? Any number of supply-siders who claim that tax cuts will promote prosperity or that tax increases will lead to a mass exodus. A “mark” who plays the game in hopes of winning, never realizing that it’s been rigged from the start? Unless you sit in the uppermost tax bracket, the mark is likely you.

Tax shifts lower one tax and increase another in a way that is purportedly revenue neutral. All too often, such proposals reduce taxes for top earners and stick low- and middle-income people with the bill by increasing regressive, consumption taxes. As ITEP’s Who Pays report shows, every state tax system asks more of the poorest residents than they do of the rich. Tax shifts allow elected officials to serve political goals, posing as fiscal stewards acting in the public interest even though their tax policies are detrimental to state budgets and critical programs such as education, infrastructure and public safety.

There is a right way to do a tax shift. Last year, the District of Columbia broadened its sales tax base to include more services used by businesses and well-off residents. At the same time, it lowered taxes for middle-income earners and strengthened the Earned Income Tax Credit to put more money in the pockets of working people. Unfortunately, states currently considering tax shifts are focused on cutting taxes for the highest-income households.

Below are the top tax shift trends that ITEP is following in legislatures across the country:

1) Hiking Taxes on Low Income Families to Pay for Tax Cuts for Wealthy Families

Ohio: Gov. John Kasich’s budget includes yet another massive tax shift away from well-off taxpayers to the middle-class and working poor. He wants to slash income taxes for the second time since he’s been in office, cutting rates by 23 percent over two years, with an immediate 15 percent cut in 2015. The cuts would cost an estimated $4.6 billion in revenue over the biennium. Kasich also wants to eliminate the income tax for business owners with $2 million or less in annual receipts at a two-year cost of $700 million dollars, and increase the personal exemption allowed for those with $80,000 or less in annual income. He would pay for these massive income tax cuts through regressive tax hikes. The governor wants to increase the sales tax rate from 5.75 to 6.25 percent and broaden the sales tax base to include a number of additional services. He also wants to increase excise taxes on cigarettes and other tobacco products, two measures that hit low-income households the hardest. ITEP ran an analysis of the tax shift plan and found that the top one percent of Ohio taxpayers would receive an average tax break of $12,010, while the bottom 40 percent of taxpayers would actually see their taxes go up by about $50. For more on the ITEP analysis read this report from Policy Matters Ohio.

Maine: Gov. Paul LePage has proposed a sweeping tax shift package that would hike sales taxes to help pay for significant personal and corporate income tax cuts and would also eliminate the estate tax. All together, the governor’s tax changes would cost $260 million when fully phased in. LePage wants to increase the sales tax rate and broaden the tax base to include some services. His plan would also eliminate cost-sharing with local governments, which could force them to hike property taxes. The governor described his plan as a way to move the state from an income-based tax system to a “pay-as-you-go” consumption-based tax system – a dangerous and ill-advised shift in the way Maine funds its crucial public investments. But, wait; there’s more! In his State of the State address, LePage announced his intention to fully eliminate Maine’s income tax in three steps (we saw how that worked out for Kansas). Eliminating the state income tax would result in the loss of half of the state’s $3 billion in annual revenue, necessitating deep cuts and major tax shifts to more recessive revenue sources.

Idaho (updated 4/6/2015): Idaho lawmakers have given serious thought to a number of tax shifting ideas, almost all of which would make the state’s regressive tax system even more unfair. The House recently decided to move forward with some of these ideas, passing a bill that would have flattened the income tax for many taxpayers, raised the gasoline tax, eliminated the Grocery Credit Refund, and exempted groceries from the sales tax. ITEP found that the overall impact (PDF) of these changes would be higher taxes for low- and middle-income taxpayers, and dramatically lower taxes for the affluent (the top 1 percent of earners would receive an average benefit of $5,000 per year). Fortunately, the Senate killed the bill and seems to be interested in refocusing on the original objective that inspired it: raising money for transportation.

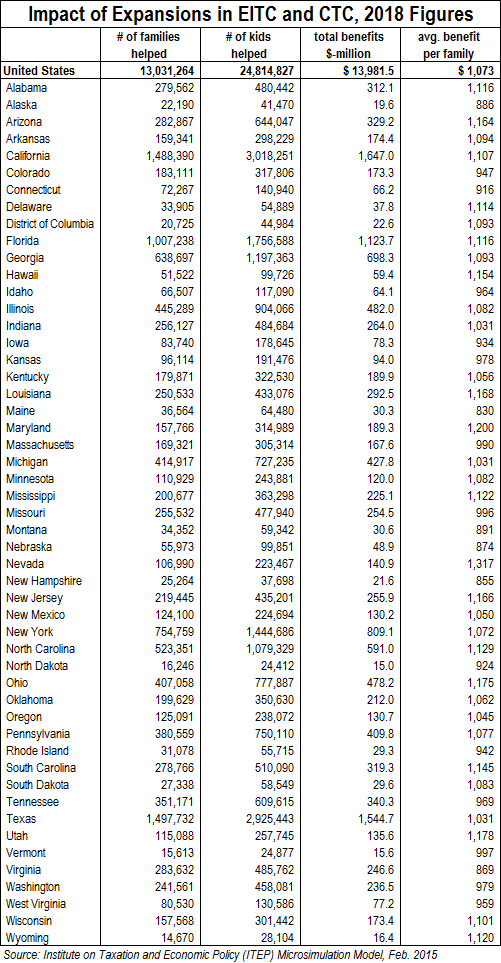

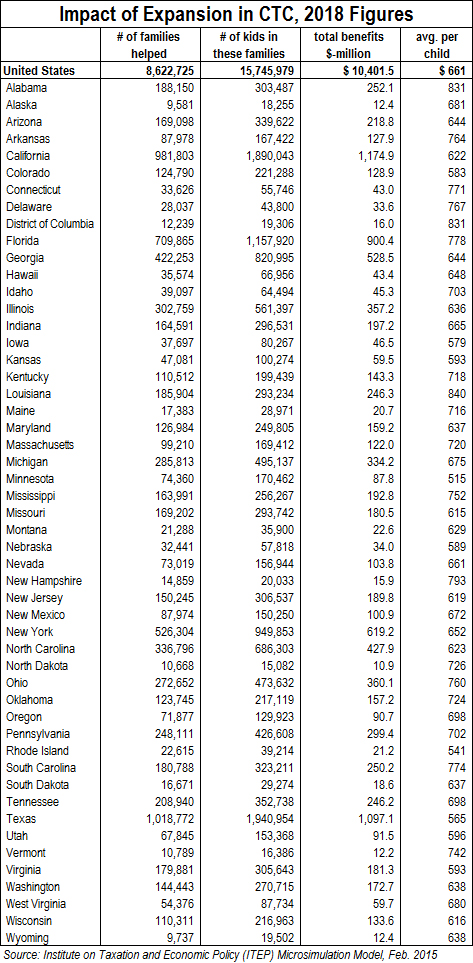

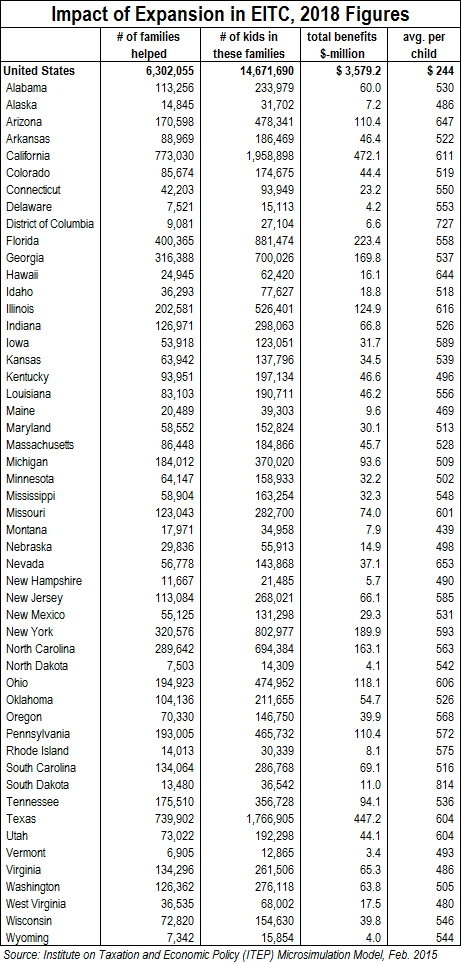

Michigan: This May, Michigan voters will be asked to approve a major tax package that would boost funding for transportation and education by some $1.7 billion per year. The package relies entirely on regressive tax changes to raise revenue, notably through a 1 percent sales tax increase and a gasoline tax restructuring that would raise the tax rate by roughly 12 cents per gallon. However, the package also includes a valuable progressive offset for low-income families in the form of a significant expansion to the state’s Earned Income Tax Credit (EITC), from 6 to 20 percent of the federal credit. Unfortunately, lawmakers are now sending signals that if voters approve this package, they may squander some of the revenues on a personal income tax cut that would be no good for the state’s economy and would make the state’s regressive tax system even more unfair. According to an ITEP analysis provided to the Michigan League for Public Policy, the income tax rate cut under consideration would give low-income taxpayers an average reduction of $12 per year, while handing over $2,600 per year to each of Michigan’s top 1 percent of earners.

2) Using Tax Shifts as Political Cover to Raise Revenue to for Infrastructure

South Carolina: Gov. Nikki Haley has said that she won’t support a gas tax increase without an across the board income tax cut. Raising gas taxes while cutting income tax rates would result in a tax shift from well-off South Carolinians to middle income and working families. Her proposal would phase in income tax rate reductions over 10 years, resulting in a top income tax rate cut from 7 to 5 percent, and increase the gas tax from 16 to 26 cents. This shift away from progressive income taxes coupled with a regressive gas tax hike would be problematic for state coffers over the long term, and low-income folks would undoubtedly feel the brunt of this tax shift.

New Jersey: Lawmakers in New Jersey seem to agree that the state is facing a transportation funding crisis and that an increase in the gas tax is needed. However, it appears more and more likely that a gas tax increase will not be enacted without a tax cut elsewhere. The taxes lawmakers are considering reducing or even eliminating to get the much needed gas tax boost? The estate and inheritance taxes, which only impact roughly 4 percent of New Jersey families each year and have zero connection to the need to boost transportation funding in the state. As our friends at New Jersey Policy Perspectives have argued, the other problem with this proposal is that it does nothing to help low- and moderate- families who will actually be hit hardest by a gas tax increase. Restoring the state’s Earned Income Tax Credit to 25 percent of the federal (cut to 20 percent in 2010) makes much more sense as the tax cut to propose alongside a gas tax hike, rather than eliminating taxes which benefit only the wealthiest families in the state.

3) Other States to Watch

Arizona: Online shoppers In Arizona (and every other state) often fail to pay sales taxes because e-retailers shirk their tax collection responsibilities. In 2013 the U.S. Senate passed legislation that would have closed this gap in sales tax enforcement, but the House failed to act on it. Now, some Arizona lawmakers say that if the federal government ever does act on this important issue that any additional revenue collected through improved enforcement should be immediately sent back out the door in the form of a regressive income tax cut. Fortunately, legislation aimed at accomplishing this end was recently voted down by a narrow margin in the Arizona House, though the sponsor is still trying to find a way to resurrect the proposal.

Mississippi (updated 4/6/2015): Mississippi lawmakers showed zeal this session for changing the state’s tax code. Gov. Phil Bryant recommended a nonrefundable Earned Income Tax Credit and Lt. Governor Tate Reeve’s proposal would have cut personal and corporate income tax rates and eliminated the state’s franchise tax. But, the most extreme plan emerged from the House where members passed a bill that would have phased out the state’s personal income tax over several years with more than two-thirds of the cut flowing to the richest 20 percent of taxpayers in the state at a cost of nearly $2 billion. Thanks in part to ITEP’s number crunching on all of the plans, which advocates in Mississippi shared with the media and lawmakers and put to use in publications, the House and Lt. Governor’s tax cutting proposals failed to muster enough support to move forward this session.

New Mexico: We are closely following a bill in the New Mexico legislature that would eliminate most of the taxes currently levied in the Land of Enchantment and replace the revenues with a 1 percent tax on gross receipts. Similar tax-shifting legislation was introduced in 2013 and gained little traction.

4) The Cautionary Tale: Kansas

Kansas: The most notorious case of tax shifting continues to unfold in Kansas. In 2012 and 2013 Gov. Brownback pushed through two rounds of very regressive income tax cuts that lowered taxes on wealthy Kansans while hiking taxes on low-income Kansans, and he’s now proposing more regressive tax hikes to help balance the state’s budget. The income tax cuts already passed will cost Kansas $5 billion in lost revenue over the next seven years. Given the state’s budget situation, Brownback has been forced to delay further income tax cuts planned for this year. He also has been forced to raise taxes, though not the ones you would think: his budget proposal would increase the excise tax on cigarettes by nearly 300 percent, from $0.79 to $2.29 per pack, and taxes on liquor would rise from 8 percent to 12 percent. The governor’s regressive tax hikes would fall on the same Kansans hurt the most by his failed economic stewardship. They also drive home some of the consequences that could arise from other officials’ rosy tax shift plans. Aggressive tax shifts that favor businesses and the wealthy at the expense of low- and middle-income families can result in states having difficulty adequately funding basic public obligations over the short and long-term.

Political nerds and TV binge watchers of all stripes will gather around the TV (or laptop) this weekend to watch the much anticipated release of Season 3 of the Netflix original series House of Cards. While the show follows the shadowy manipulations of Frank Underwood, the company and producers behind the show have done some manipulating of their own to get millions in generous tax breaks from the state of Maryland for the production of its third season.

Political nerds and TV binge watchers of all stripes will gather around the TV (or laptop) this weekend to watch the much anticipated release of Season 3 of the Netflix original series House of Cards. While the show follows the shadowy manipulations of Frank Underwood, the company and producers behind the show have done some manipulating of their own to get millions in generous tax breaks from the state of Maryland for the production of its third season.

Another year, another pass from the federal income tax for the profitable California-based utility giant Pacific Gas & Electric (PG&E).

Another year, another pass from the federal income tax for the profitable California-based utility giant Pacific Gas & Electric (PG&E).