July 7, 2016 09:00 AM | Permalink | ![]()

Read the ‘Earnings Stripping’ Letter in PDF

Read the ‘Serial Inverter’ Letter in PDF

Citizens for Tax Justice (CTJ) submitted comments this week in support of two parts of the Treasury’s proposed anti-inversion rules, the Serial Inverter Rule and the Earnings Stripping Rule, while also urging Treasury to take additional action to curb corporate inversions.

COMMENTS TO THE U.S. TREASURY DEPARTMENT AND THE INTERNAL REVENUE SERVICE ON THE PROPOSED “SERIAL INVERTER” RULE

Docket Name: Inversions and Related Transactions (REG-135734-14)

Docket ID: IRS-2016-0015-0002

Docket RIN: 1545-BM45

Dear Secretary Lew,

Citizens for Tax Justice is a nonpartisan public interest research and advocacy organization fighting to give American citizens a greater voice in tax laws at the federal, state and local levels. We have frequently spoken out against the practice of corporate tax inversions, which occur when a U.S. company, upon merging with a foreign company, reincorporates itself as a foreign entity and escapes paying U.S. taxes. The Joint Committee on Taxation estimates that corporate inversions could result in a loss to Treasury of $34 billion over the next 10 years; this money could be spent to improve the lives of countless Americans. As a public interest organization, we believe that the American taxpayer should not have to make up for the revenue loss created by this kind of corporate misbehavior.

We strongly support the proposed rule on Inversions and Related Transactions (Docket ID: IRS-2016-0015-0002), also known as the “serial inverter” rule. This action will prevent multinational corporations from circumventing current anti-inversion regulations by engaging in multiple inversions in a three-year period. This proposed new rule will take an important step toward putting an end to offshore tax avoidance.

We’ve already seen the positive impact of the proposed serial inverter rule in the case of Pfizer, which abandoned its planned $125 billion merger with Allergan shortly after the rule was proposed. This action alone may have saved U.S. taxpayers as much as $40 billion in taxes on offshore profits that Pfizer could have avoided by inverting and will likely prevent billions more revenue losses in the future by preventing other companies from inverting.

While curbing the abuse of serial inverters will undoubtedly help ameliorate the problem of corporate tax avoidance and inversions, further steps can be taken. The Treasury Department should go beyond the scope of this rule to prevent “hopscotch loans,” which occur when inverted U.S. companies escape paying taxes on dividends by loaning to a foreign parent, bypassing the U.S. parent. As we’ve noted in a previous letter, Treasury should expand on its prior Notice 2014-52 by further limiting the ability of inverted firms to use these hopscotch loans and to decontrol their foreign parent companies to avoid taxation. It should do so by applying its rules to all expatriating companies, or at least to those which maintain 50 percent ownership by the original shareholders of the U.S. firm. There is no reason to link these rules to section 7874 (which sets 60 percent as the threshold) considering the broad authority that Treasury has in Section 956.

A recent study by Citizens for Tax Justice found that U.S. companies likely owe up to $695 billion in taxes on the $2.4 trillion in earnings that they stash offshore. The amount held offshore, and thus the amount companies are avoiding in taxes, grows by hundreds of billions of dollars each year. This must end. In the absence of Congressional action to fix this problem, Treasury should take every possible step to prevent the base erosion and profit shifting created by corporate tax inversions and other corporate tax avoidance.

Thank you for your careful consideration of these comments.

Sincerely,

Robert S. McIntyre

Director of Citizens for Tax Justice

COMMENTS TO THE U.S. TREASURY DEPARTMENT AND THE INTERNAL REVENUE SERVICE ON THE PROPOSED “EARNINGS-STRIPPING” RULE

JULY 7, 2016

Docket Number: IRS-2016-0014-0002

Docket Name: Treatment of Certain Interests in Corporations as Stock or Indebtedness (REG-108060-15)

Docket RIN: 1545-BN40

Dear Secretary Lew,

Citizens for Tax Justice is a nonpartisan public interest research and advocacy organization fighting to give American citizens a greater voice in tax laws at the federal state and local levels. We have frequently spoken out against the practice of corporate tax inversions, which occur when a U.S. company, upon merging with a foreign company, reincorporates itself as a foreign entity and escapes paying U.S. taxes. While inversions have recently drawn public attention, the overall cost of offshore corporate tax avoidance is enormous. One recent estimate found that profit shifting costs the United States over $100 billion per year. As a public interest organization, we believe that the American taxpayer shouldn’t have to make up for the revenue hole created by this kind of corporate misbehavior.

We strongly support the proposed rule on Treatment of Certain Interests in Corporations as Stock or Indebtedness, also known as the “earnings stripping” rule. By inhibiting multinational corporations’ ability to artificially shift profits out of their U.S. affiliates through the use of debt, this proposed action would take an important step toward putting an end to offshore tax avoidance.

Earnings stripping is an accounting gimmick used by multinational corporations to avoid taxes by shifting profits from higher- to lower-tax jurisdictions. This practice usually involves companies giving their subsidiaries in higher-tax jurisdictions (like the United States) loans from subsidiaries in low or zero tax jurisdictions (like Bermuda or Ireland). The interest payments on these loans are tax-deductible in the higher-tax country and are paid out to the subsidiary in the lower-tax country, thus allowing the company to artificially shift a substantial amount of income from the higher- to the lower-tax jurisdiction.

For a U.S.-based company, earnings stripping is nominally limited by the fact that if the company wants to repatriate its offshore profits back to the United States it will have to pay taxes on them. To escape this sensible limitation, some U.S. companies have sought to engage in inversions so that they will never have to pay taxes on any of the money shifted offshore.

Because earnings stripping is a common practice among multinational corporations, we applaud the fact that the rule applies not only to inverted companies, but to all multinationals doing business in the United States. Cracking down on all earnings stripping activities will raise much-needed revenue, and will also help level the playing field between multinational corporations that can take advantage of earnings stripping and the many smaller domestic businesses that cannot.

While curbing the abuse of earnings stripping will undoubtedly help ameliorate the problem of corporate tax avoidance and inversions, further steps can be taken. The Treasury Department should go beyond the scope of this rule to prevent “hopscotch loans,” which occur when inverted U.S. companies escape paying taxes on dividends by loaning to a foreign parent, bypassing the U.S. parent. As we’ve noted in a previous letter, Treasury should expand on its prior Notice 2014-52 by further limiting the ability of inverted firms to use these hopscotch loans and to decontrol their foreign parent companies to avoid taxation. It should do so by applying its rules to all expatriating companies, or at least to those that maintain 50 percent ownership by the original shareholders of the U.S. firm. There is no reason to link these rules to section 7874 (which sets 60 percent as the threshold) considering the broad authority the Treasury has in Section 956.

A recent study by Citizens for Tax Justice found that U.S. companies likely owe up to $695 billion in taxes on the $2.4 trillion in earnings that they stash offshore. The amount held offshore, and thus the amount these companies are avoiding in taxes, grows by hundreds of billions of dollars each year. This must end. In the absence of Congressional action to fix this problem, Treasury should take every possible step to prevent the base erosion and profit shifting created by corporate tax inversions and other corporate tax avoidance.

Thank you for your careful consideration of these comments.

Sincerely,

Robert S. McIntyre

Director of Citizens for Tax Justice

Want even more CTJ? Check us out on Twitter, Facebook, RSS, and Youtube!

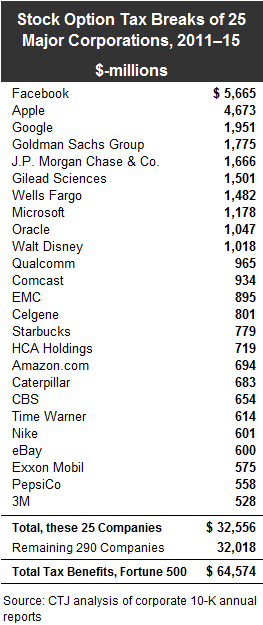

Apple & Facebook Biggest Beneficiaries

Apple & Facebook Biggest Beneficiaries