The theory that tax cuts for the affluent will eventually trickle down to everyone else is shopworn, yet supply-side adherents keep promising the public that the rich can have their tax cuts and the rest of us will eat cake too.

Despite 35 years of data showing this to be false, the notion has seduced enough policymakers to keep the lights on at Art Laffer’s house.

At least 10 states have tax cut proposals in motion that, unlike the tax shifts we reviewed previously, will not offset cuts by raising other taxes but by raiding surpluses or reducing spending. The overwhelming majority of these proposals will reduce taxes for the best off while doing nothing or little for everyone else, making a regressive tax landscape worse. Gov. Asa Hutchinson’s overhaul of his state’s income tax and Mississippi Gov. Phil Bryant’s proposal to introduce a state Earned Income Tax Credit (EITC) would actually benefit low- and moderate-income families, but most of the other proposals would lead mainly to benefits for the wealthy.

Over time such tax cuts exacerbate income inequality and stymie opportunity for the masses. Taxes and spending are on a balance scale. Top-heavy tax cuts and their purported economic benefits do not trickle down a rolling hill; they tip the scale in favor of the rich while depriving states of necessary revenue to adequately fund basic services, including education, public safety, infrastructure health and other priorities. Below are some pending proposals:

Arkansas: Gov. Asa Hutchinson fulfilled his campaign promise of passing a middle class tax cut. The governor’s plan introduces a new income tax rate structure for middle income Arkansans. To help pay for the measure the capital gains exemption was reduced from 40 to 50 percent. Using data from ITEP, Arkansas Advocates for Children and Families explains that the taxpayers who benefit from capital gains exemptions are wealthier families.

Florida: Once again, Florida Gov. Rick Scott is pushing lawmakers to enact an unusual hodgepodge of tax cuts. Under his proposal, taxes on cable TV and cell phone usage would drop by 3.6 percentage points, manufacturing machinery and textbooks would both be exempted from the sales tax, the corporate income tax exemption would be raised from $50,000 to $75,000, and yet another back-to-school sales tax holiday would be held this summer. The overall cost of this package would be roughly $700 million, and while it’s too early in the session to gauge the chances of passage, there is apparently some skepticism toward the plan in the state legislature.

Idaho: The big tax shift sought by some Idaho lawmakers is off the table for now, but Gov. Butch Otter made clear all along that he prefers a straight-up cut to the state’s corporate income tax rate, and its top personal income tax rate, from 7.4 to 6.9 percent. Our analysts recently found that such a tax cut would make Idaho’s decidedly regressive tax system even more unfair. More than three out of every four dollars in personal income tax cuts would flow to the wealthiest 20 percent of households, and members of the top 1 percent would see an average tax cut of over $3,500 each year. These cuts would come on top of a very similar package of regressive income tax reductions enacted in 2012.

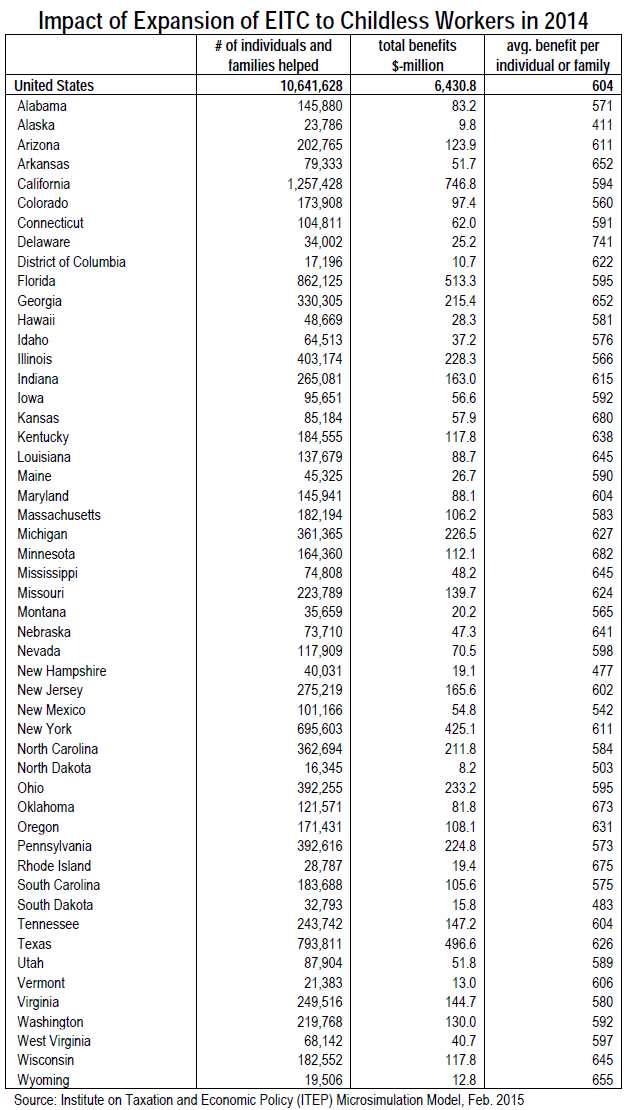

Mississippi: Lawmakers in the Magnolia State can’t seem to get enough of tax cut proposals. In addition to the tax shift proposal passed by the House recently (and written about here), lawmakers are debating a variety of tax cutting measures, which include decreasing personal and corporate income tax rates, introducing a nonrefundable EITC, and eliminating the corporate franchise tax.

Montana: The Montana legislature has approved a bill that would cut personal income tax rates across the board and reduce state revenues by roughly $42 million per year. ITEP analyzed similar, earlier versions of the cut and found that high-income households would be the largest beneficiaries and that low-income and middle-income taxpayers, who currently face the highest overall state and local tax rates, would receive little or no benefit. Governor Steve Bullock is likely to veto the plan because of its impact on the state’s ability to fund vital public services.

Nebraska: With the sheer number and diversity of tax cut bills circulating in Nebraska this winter, it seems certain some cut will be enacted. Much of the focus so far has been on reducing property taxes, a stated priority of newly elected Gov. Pete Ricketts. Property tax proposals include creating a new refundable, targeted property tax circuit breaker credit for homeowners and renters, introducing a local income tax to reduce reliance on property taxes for school funding, hiking the sales tax rate to pay for a bump in a statewide property tax credit, and increasing personal and corporate income tax rates to pay for property tax cuts. State business leaders, however, have made it clear that income tax cuts are their main concern, and Governor Ricketts has not ruled out the possibility. One plan being floated would reduce personal and corporate income tax rates over eight years, giving the biggest benefits by far to the richest Nebraskans.

North Carolina (updated 4/6/2015): Two years after North Carolina enacted a sweeping tax cut package, state lawmakers have returned this year with more tax cutting plans that will bust the budget to benefit wealthy residents and profitable corporations. Senate Republicans have unveiled another round of personal income tax cuts that cost more than $1 billion when fully enacted and would slash millions of dollars in corporate income taxes. There has also been talk of reducing taxes on capital gains income, restoring items eliminated in 2013 including a deduction for medical expenses and historic preservation tax credit. What makes these proposals even more egregious is the state’s anticipated revenue shortfall of almost $300 million this year. Lawmakers were forced to close a $500 million revenue gap last year with deep spending cuts after underestimating the steep cost of the tax cuts passed in 2013.

North Dakota: Just a few short months ago, North Dakota lawmakers were giddy about the idea of using booming oil and gas tax revenue to pay for an elimination or significant reduction of the state’s personal income tax. But as gas prices plummeted, reality set in and the House approved a scaled back proposal – a 10 percent across-the-board reduction in personal and corporate income tax rates (Gov. Dalrymple also proposed a 10 percent personal income tax cut). North Dakota lawmakers enacted similar plans in 2011 and 2013, slowly chipping away at the two taxes.

Tennessee: In what’s becoming an annual tradition, multiple Tennessee lawmakers have proposed (subscription required) repealing the state’s “Hall Tax”—a modest 6 percent income tax on interest, dividends, and capital gains income. As we showed in our recent Who Pays? report, the Hall Tax is a rare progressive bright spot in a tax system that tilts overwhelmingly in favor of affluent households. Fortunately, leaders in the state’s House and Senate are reportedly unenthused by the idea since Tennessee’s wealthiest households recently benefited from cuts in estate, inheritance, and gift taxes. And while it’s discouraging that the governor isn’t making principled tax fairness arguments against these proposals, he is very skeptical that the state can afford to get rid of the Hall Tax right now.

Texas: Lawmakers in the Lone Star State hope to enact a tax cut package that would cost about $4 billion over a two year period. Governor Greg Abbott’s top priority is cutting the business franchise tax, and he has said that he will veto any budget that does not include such a cut. So far, the main options for reducing business franchise taxes include cutting the rate from 1 to 0.85 percent or raising the exemption from $1 million to $4 million. The governor would also like to see school property taxes cut, and the Senate seems happy to go along with that idea. Options currently under discussion include raising the $15,000 homestead exemption to $33,625, or converting it to equal 25 percent of home value. As we explain in this policy brief, the percentage-based option is less fair than a flat-dollar exemption. But it’s also important to keep in mind the context provided by Dick Lavine of the Center for Public Policy Priorities: “There’s better uses of this money … than tax cuts.”

Ryan’s plans typically called for taking bold steps to reduce the federal budget deficit by eliminating tax “loopholes,” but were utterly silent on the question of whose ox should be gored in this process. By answering the easy questions (how far income tax rates should be cut) and refusing to even touch the hard ones (which loopholes should be closed), Ryan’s budget plans made budget-busting, highly regressive tax proposals the main topic at budget time each year.

Ryan’s plans typically called for taking bold steps to reduce the federal budget deficit by eliminating tax “loopholes,” but were utterly silent on the question of whose ox should be gored in this process. By answering the easy questions (how far income tax rates should be cut) and refusing to even touch the hard ones (which loopholes should be closed), Ryan’s budget plans made budget-busting, highly regressive tax proposals the main topic at budget time each year.

Xerox is not alone in undercutting the Roundtable’s case for corporate tax cuts. Our February 2014 magisterial survey of tax avoidance by profitable Fortune 500 corporations found that the Business Roundtable’s

Xerox is not alone in undercutting the Roundtable’s case for corporate tax cuts. Our February 2014 magisterial survey of tax avoidance by profitable Fortune 500 corporations found that the Business Roundtable’s

The tax break in question, the “active financing exception,” has come back from the dead before. Repealed as part of the loophole-closing Tax Reform Act of 1986, Congress temporarily reinstated the active financing exception in 1997 after fierce lobbying by GE and other multinational financial companies. Since then, lawmakers have extended it numerous times, usually for one or two years at a time and often retroactively.

The tax break in question, the “active financing exception,” has come back from the dead before. Repealed as part of the loophole-closing Tax Reform Act of 1986, Congress temporarily reinstated the active financing exception in 1997 after fierce lobbying by GE and other multinational financial companies. Since then, lawmakers have extended it numerous times, usually for one or two years at a time and often retroactively. A decade and a half ago, the federal government was running a surplus, the economy was humming along, poverty had continually declined for the previous seven years, and the Republican candidate for president essentially told the nation we could cut taxes and maintain the status quo.

A decade and a half ago, the federal government was running a surplus, the economy was humming along, poverty had continually declined for the previous seven years, and the Republican candidate for president essentially told the nation we could cut taxes and maintain the status quo.