The first and only Vice Presidential Debate of the election season between Vice President Joe Biden and Wisconsin Congressman Paul Ryan featured a spirited discussion over their competing visions for tax policy. While watching, we began to genuinely wonder if Biden had spent time reading Citizens for Tax Justice (CTJ) materials considering that time and again he made precisely the points CTJ has been making for years. Ryan, on the other hand, repeatedly misrepresented the tax system and the two tickets’ tax plans.

Below we breakdown the most important tax policy moments in the debate:

1. Biden Highlights the Regressiveness of Extending All the Bush Tax Cuts

1. Biden Highlights the Regressiveness of Extending All the Bush Tax Cuts

While the presidential candidates largely ignored the Bush tax cuts in their debate last week, Biden put them front and center during the VP debate when he pointed out that Romney and Ryan are proposing the “the continuation of a tax cut that will give an additional $500 billion in tax cuts to 120,000 families” over the next ten years, compared to the Obama Administration plan for the Bush tax cuts.

Biden’s formulation here is a little confusing but not incorrect. Of course, President Obama proposes to allow the Bush income tax cuts to expire for income in excess of $250,000 for couples and in excess of $200,000 for singles, and only 2 percent of taxpayers would lose any portion of their Bush income tax cuts under this approach. The administration has stated that this would cost $849 billion less, over ten years, than extending the Bush income tax cuts for all income levels, while our own estimate is that it would cost $887 billion less over ten years. Pretty close.

Biden is focusing specifically on the part of this figure that would benefit the richest 120,000 families, apparently based on figures from the Tax Policy Center. Our own calculations essentially back up Biden’s point. We estimate that the richest taxpayers with incomes exceeding $2 million in 2013 (the richest 135,000 families in 2013) would receive about 57 percent of the income tax cuts that would otherwise expire under Obama’s approach, which comes out to $507 billion over ten years.

2. Ryan Promises the Mathematically Impossible

In defending Romney’s tax plan, Ryan reiterated their ticket’s commitment to “lower tax rates across the board” and to “close loopholes,” while simultaneously sticking to the “bottom lines” of not raising the deficit, not increasing taxes on the middle class or lowering the share of income that is borne by high-income earners. But Ryan is defending a plan that CTJ has found is mathematically impossible. Even if Romney and Ryan eliminated all the tax expenditures for wealthy taxpayers that they have put on the table, our analysis has found that their across-the-board tax cuts would still require them to give an average tax break of $250,000 to individuals making over $1 million, which would violate their pledge not to lower the share of taxes borne by high-income earners.

Ryan said during the debate that there are six studies showing that their plan is possible, but Biden correctly pointed out that even the studies Ryan cites conclude that the plan would require increasing taxes on taxpayers who do not have particularly high incomes.

3. Biden Calls Ryan Out for Taking Capital Gains Tax Breaks Off the Table

One of the major reasons that the Romney campaign’s tax plan would be incapable of eliminating enough tax expenditures to add up is that Romney has specifically said that he would keep the tax breaks for capital gains and stock dividends. During the debate, Biden noted that this shows the lack of seriousness in Romney’s loophole-targeting approach because Romney has exempted the “biggest loophole” of all – the “capital gains loophole.” As CTJ pointed out in a recent report, ending the capital gains tax preference would tremendously improve fairness, raise revenue, and simplify the tax code in one fell swoop.

4. Ryan and Biden Dispute the Definition of Small Businesses

Repeating Romney’s line on small businesses from the first presidential debate, Ryan claimed that Obama is going to raise taxes on small businesses and kill 710,000 jobs by doing so. The reality, however, is that only the 3 to 5 percent richest business owners (individuals who could hardly be called “small business” owners) would lose any of their tax breaks, and the job loss claims are complete malarkey.

5. Biden Takes on Romney and Ryan’s Commitment to Grover Norquist

During the first presidential debate, Romney reiterated his pledge to not raise a single penny in revenue, even if the revenue was raised as part of a deal that included $10 in spending cuts for every $1 in revenue increases. Biden took issue with this commitment saying that “instead of signing pledges to Grover Norquist not to ask the wealthiest among us to contribute to bring back the middle class, they should be signing a pledge saying to the middle class we’re going to level the playing field.”

Biden is absolutely right that we need to reject the extreme anti-tax approach taken by individuals like Grover Norquist and instead embrace a balanced approach to deficit reduction. The question for Romney is when he will recognize that a balanced approach is not only what the American people want, but also what business experts support as well.

6. Ryan Misrepresents History of 1986 Tax Reform

Responding to the question of what specific loopholes he and Romney are proposing to close, Ryan attempted to dodge the question by arguing that they should not lay out specific loopholes they want to close because doing so would prevent them from following the model that allowed Ronald Reagan and Tip O’Neill to produce the 1986 tax reform. The reality, however, as recounted by CTJ Director Bob McIntyre – whose work was integral to the passage of the 1986 reform – is that Reagan’s Treasury Department released a detailed tax reform plan explicitly laying out exactly which tax expenditures the Administration would like to see closed. In other words, the 1986 tax reform experience actually proves the opposite of what Ryan is saying about vagueness being some kind of asset.

7. Biden Revives Romney’s 47% Remark

Continuing his efforts to upend tax myths during the debate, Biden took issue with Romney’s earlier statement that 47 percent of Americans aren’t paying their fair share, and he noted that many middle income people actually “pay more effective tax than Governor Romney in his federal income tax.” Biden was right to push back against the notion that any Americans are not contributing their fair share since, on average, any American’s share of total taxes is already roughly equal to their share of total income. In addition, CTJ has found that individuals making around $60,000 do in fact pay an effective federal tax rate of 21.3% on average, which is a lot compared to Romney’s tax rate of 14% in 2011.

8. Ryan Claims Obamacare Includes 12 Middle Class Tax Hikes

During the debate, Ryan asserted, “Of the 21 tax increases in Obamacare, 12 of them hit the middle class.” The reality, according to a CTJ analysis, is that 95 percent of the tax increases included in the healthcare reform legislation would be borne by either companies or households making over $250,000. Adding to this, Ryan’s specific point about the 12 tax provisions is mostly false because 4 of the 12 provisions are not really taxes at all.

9. Biden Stumbles on the Primary Cause of Great Recession

The only significant tax policy stumble for Biden came when he argued that Ryan helped create the Great Recession by “voting to put two wars on a credit card, to at the same time put a prescription drug benefit on the credit card, a trillion-dollar tax cut for the very wealthy.” The problem of course is that the Great Recession was due primarily to a financial crisis, not some sudden crisis in government spending and deficits.

While extraordinary increases in deficit spending and tax cuts for the rich during President George W. Bush’s presidency, (which Ryan did vote for), did not cause the recession, they certainly caused an explosion in the national debt. In fact, if continued, the Bush tax cuts and the cost of the wars will account for nearly half of the public debt by 2019.

10. Ryan Wrong on How Much Revenue Could Be Raised by Taxes on the Rich

In an attempt to discredit the idea that allowing the Bush tax cuts to expire for the wealthiest Americans will help fix the deficit, Ryan argued that “if you taxed every person and successful business making over $250,000 at 100 percent, it would only run the government for 98 days.” To start, the entire premise of this argument is bogus because the Obama administration is not proposing a revenue-only approach to deficit reduction; in fact it has already signed into law over $2 trillion in spending cuts. In addition, Ryan ironically failed to discern, even by his own calculations, that 98 days worth of government spending would be more than enough to close the projected budget deficits and would be more than enough to pay down the national debt in the coming years.

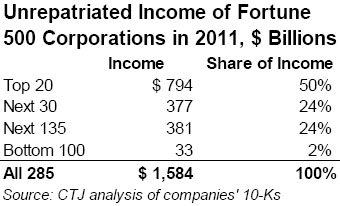

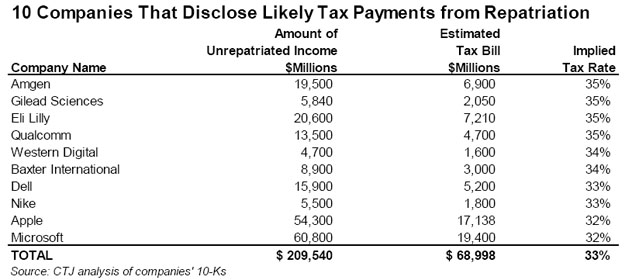

While the presidential candidates debate whether the tax code rewards companies that move operations overseas, a new CTJ report shows that ten companies, including Apple and Microsoft, indicate in their own financial statements that most of their foreign earnings have never been taxed – anywhere. The statements the companies file with the SEC reveal that if they brought their foreign profits back to the U.S., they would pay the full 35 percent U.S. tax rate, which is how we can surmise that no foreign taxes were paid that would offset any of the 35 percent U.S. tax rate.

While the presidential candidates debate whether the tax code rewards companies that move operations overseas, a new CTJ report shows that ten companies, including Apple and Microsoft, indicate in their own financial statements that most of their foreign earnings have never been taxed – anywhere. The statements the companies file with the SEC reveal that if they brought their foreign profits back to the U.S., they would pay the full 35 percent U.S. tax rate, which is how we can surmise that no foreign taxes were paid that would offset any of the 35 percent U.S. tax rate. In last night’s presidential debate, Governor Romney pointed out that President Obama’s pension holds investments in Chinese companies and even in a Cayman Islands trust. Unlike Romney’s self-directed

In last night’s presidential debate, Governor Romney pointed out that President Obama’s pension holds investments in Chinese companies and even in a Cayman Islands trust. Unlike Romney’s self-directed  During Tuesday night’s presidential candidate

During Tuesday night’s presidential candidate  In particular, our analysis shows that ten corporations, representing over a sixth of the $1.5 trillion in unrepatriated profits, reveal sufficient information to show that they have paid little or no tax on their offshore profit hoards to any government. That implies that these profits have been artificially shifted out of the United States and other countries where the companies actually do business, and into foreign tax havens.

In particular, our analysis shows that ten corporations, representing over a sixth of the $1.5 trillion in unrepatriated profits, reveal sufficient information to show that they have paid little or no tax on their offshore profit hoards to any government. That implies that these profits have been artificially shifted out of the United States and other countries where the companies actually do business, and into foreign tax havens.

When Kansas Governor Sam Brownback signed into law a

When Kansas Governor Sam Brownback signed into law a  As ITEP’s Meg Wiehe explained it to the

As ITEP’s Meg Wiehe explained it to the  All revenues from Proposition 38 would go directly to K-12 schools and only K-12 schools. None of the revenue could be spent on any other budget priorities since it can only supplement rather than supplant current spending on K-12 education; however, about a third of the funds can be used to reduce state debt. Even with the billions of dollars in new revenue Proposition 38 would bring to the Golden State, if it gets more votes than Proposition 30, $6 billion in spending cuts would automatically go into effect as per the Governor’s budget, forcing reductions in vital programs such as community colleges, universities, corrections and others.

All revenues from Proposition 38 would go directly to K-12 schools and only K-12 schools. None of the revenue could be spent on any other budget priorities since it can only supplement rather than supplant current spending on K-12 education; however, about a third of the funds can be used to reduce state debt. Even with the billions of dollars in new revenue Proposition 38 would bring to the Golden State, if it gets more votes than Proposition 30, $6 billion in spending cuts would automatically go into effect as per the Governor’s budget, forcing reductions in vital programs such as community colleges, universities, corrections and others.