February 11, 2016 03:25 PM | Permalink | ![]()

Earlier this week, President Barack Obama released details of his proposed federal budget for the fiscal year ending in 2017. While many cynical observers and some members of Congress immediately derided the budget blueprint as an irrelevant exercise in political theatre, the President’s plan actually includes a number of sensible ideas that could help point the way to meaningful federal tax reform in years to come. Here’s a quick overview of the best—and the rest—of the tax policy ideas in the Obama 2017 budget plan.

The President’s proposed budget includes $3.2 trillion in tax increases over the next ten years, most of which would fall primarily on the wealthiest individual taxpayers and on corporations. Obama proposes to use about $400 billion of those tax hikes to pay for targeted tax cuts, primarily for middle- and low-income families, and would use the rest to pay for needed public investments and to reduce the deficit.

Where the Money Comes From

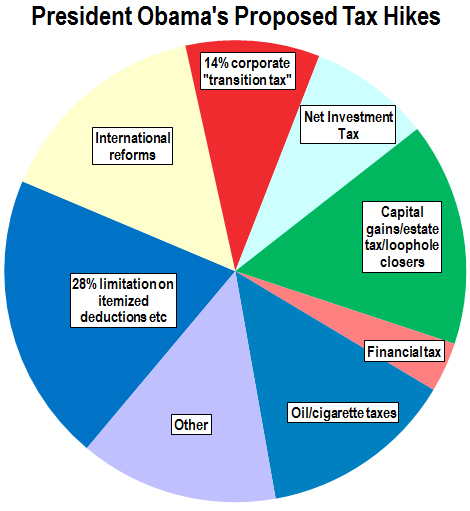

President Obama’s budget would raise about $3.2 trillion in new tax revenues over the next ten years from a diverse set of sources, primarily affecting wealthier taxpayers and large corporations, but also including an “oil fee” and a cigarette tax hike that would have an impact on middle- and low-income families.

President Obama’s budget would raise about $3.2 trillion in new tax revenues over the next ten years from a diverse set of sources, primarily affecting wealthier taxpayers and large corporations, but also including an “oil fee” and a cigarette tax hike that would have an impact on middle- and low-income families.

Roughly 15 percent of the new revenues in Obama’s proposal would come from a variety of proposals designed to pare back tax benefits accruing to wealthy investors. Most notably, the President would increase the top tax rate on capital gains to 28 percent, revitalize the estate tax by increasing the top rate, end the “stepped up basis” tax break that allows many wealthy investors to avoid any tax on their capital gains, and repeal the “carried interest” loophole that allows hedge fund managers to characterize income as capital gains.

Another fifth of the revenue-raisers would come from a single provision, known as the “28 percent limitation,” that would limit the value of itemized deductions and other tax breaks to 28 cents for each dollar deducted. This would affect only taxpayers currently paying federal tax rates above 28 percent. (In 2016, this means couples making more than $250,000.) This reform is similar to proposals the president has included in previous budgets.

The budget includes two revenue-raising proposals that would affect corporations: a one-time “transition tax” on U.S.-based corporations holding profits offshore for tax purposes, and a low-rate tax on the liabilities of the very largest financial companies.

The president’s budget also includes two tax changes that would fall primarily on low- and middle-income families: a $10.25 per barrel “oil fee” and an increase in the federal tobacco tax. This would represent about one sixth of the tax hikes included in the Obama budget blueprint.

Where the Money Goes

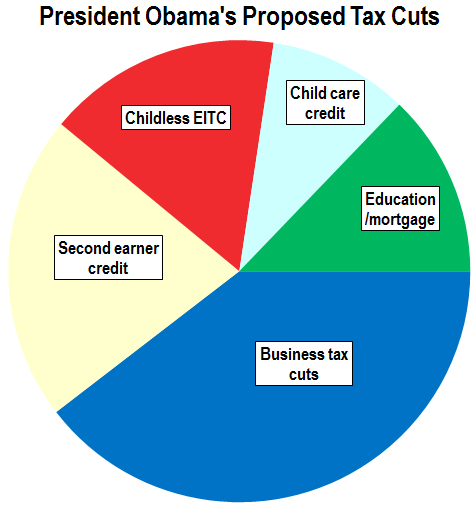

The president’s budget would set aside about ten percent of the revenues from his proposed tax increases to cut taxes. Forty percent of these tax cuts would be targeted to businesses, with the remainder designed to benefit middle- and low-income working families.

The president would also fill one of the most glaring gaps in the structure of the EITC: its low benefits for childless workers. The budget would double the maximum benefit of this wage subsidy for low-income single workers.

Tax Reform Ideas in the President’s Budget: The Best…

The president’s budget includes a healthy dose of new, and old, tax reform proposals. Some, like the sensible proposal to cap the benefits of itemized deductions at 28 percent, have featured prominently in previous budget proposals under President Obama’s watch. Others, notably the proposal to impose a $10.25-per-barrel fee on oil consumption, are new ideas that would take welcome steps toward a more sustainable tax system. And short-term politics aside, many of these proposals would represent a sensible starting point for tax reform blueprints in years to come.

- Closing Medicare tax loophole for pass-throughs: The “net investment income tax” enacted as part of President Obama’s health care reforms added a healthy dose of fairness—and revenue—to the tax system, imposing a 3.8 percent tax on families earning over $250,000. But the tax didn’t apply to income from pass-through entities like S corporations. To allay sensible fears that some well-heeled taxpayers are gaming the system by transforming their business into pass-through form, Obama would include pass-through income in the net investment income tax. Ending this single tax dodge is forecast to raise an astonishing $271 billion over ten years.

- Boosting wages for low-income working families: the Earned Income Tax Credit provides a vital wage subsidy for workers with children living near or below the poverty line, but generally shortchanges workers without children. The budget blueprint would reduce this inequity, doubling the maximum credit for workers without children.

- Ending “stepped up basis” for capital gains: The federal income tax has long had a loophole wealthy investors could drive a truck through: the complete forgiveness of federal income tax liability on the value of stocks and other capital assets passed on from decedents to their heirs. The president’s plan would end this tax break for heirs inheriting more than $200,000 for a married couple ($100,000 for singles). While the tax policy community has long agreed that the so-called “stepped up basis” is absurd, few elected officials have actively sought to repeal it—until now.

- Taxing wealth more like work: Current law imposes a top tax rate on capital gains that, at 23.8 percent, is well below the 39.6 percent top tax rate on wages. By hiking the top capital gains rate to 28 percent for the very best-off Americans, President Obama’s plan would at least slightly reduce the tax preference for wealth over work. Notably, even if the president’s plan were enacted, the top rate on investment income would remain fully 11.6 percent below the top rate on wages.

- Simplifying and expanding education tax credits: The President proposes to simplify and restructure the hodgepodge of education tax breaks currently allowed, expanding the middle-income American Opportunity Tax Credit and making more of this credit refundable to benefit low-income working families that don’t owe federal income taxes. Obama would also protect the future value of these credits by indexing it for inflation.

- Expanding the child care credit: Recognizing that dependent care expenses can be unaffordable for working parents, the president proposes to substantially increase an existing tax credit against child care expenses. Obama would increase the income level at which the credit begins to phase down from $15,000 to $120,000, making more middle-income families eligible for the maximum credit. Obama would also more than double the potential tax credit for families with children under the age of five.

…And the Rest

While the president’s outline of individual tax reforms would clearly be a win for tax fairness, some provisions would needlessly complicate the tax code. On the corporate side, President Obama’s proposals are more clearly geared toward raising revenues than in previous years, but still include a wasteful giveaway to the biggest offshore tax avoiders in the form of a low-rate “transition tax” on offshore cash.

- Low-rate “transition tax” on multinational corporations’ offshore cash. Faced with the prospect of large multinationals such as Apple and Microsoft avoiding U.S. tax by stashing their profits in offshore tax havens, Obama proposes a one-time, 14 percent “transition tax” on these profits, after which they will never be subject to additional U.S. tax. Apparently driven by the philosophy that something is better than nothing, Obama’s plan would, in fact, give $82 billion in tax cuts to just ten of the biggest tax avoiders. A better plan would require these companies to pay the 35 percent tax they have adeptly avoided to date.

- $10.25 per barrel “Oil Fee”. The nation’s transportation infrastructure is chronically underfunded for one simple reason: its main funding source, the federal gas tax, hasn’t been increased since 1993 and has lost much of its value since then. As in previous years, President Obama is not proposing to increase the gas tax—but this year he’s proposing a second-best alternative. Obama would levy a fee of $10.25 for each barrel of oil consumed in the United States, which amounts to an indirect tax hike not only on gasoline and diesel but a variety of other consumer items, including heating oil and plastic products. As the President’s budget proposal notes, this proposal could have a helpful effect in discouraging consumption of fossil-fuel related products, but also would impose a meaningful tax hike on low- and middle-income families.

- Reinventing the wheel: We already have a federal income tax credit designed to offset child care expenses for two-earner couples, and, as previously noted, the President sensibly wants to expand it. So his proposal to create a new “second earner” credit that doesn’t even require such couples to incur child care expenses is unnecessary and wasteful.

Want even more CTJ? Check us out on Twitter, Facebook, RSS, and Youtube!