November 23, 2015 01:15 PM | Permalink | ![]()

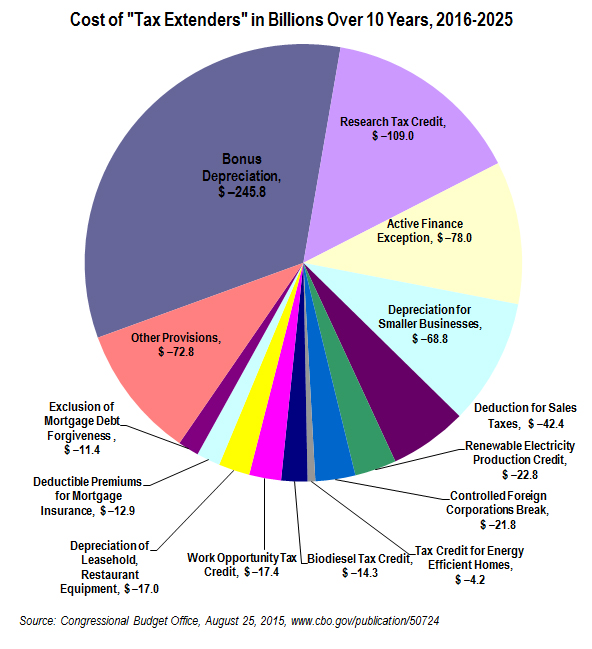

Many of the most costly tax extenders should be reformed or remain expired

Year after year, Congress has renewed a package of temporary tax provisions known as the “tax extenders.” Nearly all of them should be substantially curtailed or allowed to remain expired. Because these provisions are in the tax code and routinely evaluated as a package, the individual provisions have not been subjected to the same level of scrutiny as spending programs of comparable size.

The four most costly provisions — bonus depreciation, the research credit, the so-called “active financing exception,” and the “CFC Look-Through Rule” — make up 62 percent of the total cost of the package. Yet they are not designed to help the economy, as discussed below. Many of the other tax extenders are subsidies that could more sensibly be provided through direct spending.

Lawmakers or special interest groups often argue that the tax extender legislation should be enacted because it includes a helpful provision that benefits individuals or small businesses. For example, it’s easy to support the small deduction for teachers who purchase classroom supplies out of their own pockets. Putting aside the merits of this provision, this break makes up just 0.3 percent of the cost of the tax extenders package. This and other similarly small provisions do not justify $740 billion over 10 years in deficit-financed tax cuts that mostly go to corporations and businesses.

Bonus Depreciation

10-Year Cost: $245.8 billion

Bonus depreciation is the costliest and most wasteful tax break in the tax extenders package. It is an expansion of existing breaks that allow businesses to deduct their asset’s depreciation more quickly than is warranted by its actual decline in value. The provision was first passed early in the George W. Bush administration as a temporary economic stimulus. It has been reenacted or extended many times since then with no discernible positive effect on business investment. Instead, it provides another corporate tax loophole for many large corporations.

How does this provision work? Companies are allowed to deduct from their taxable income the expenses of running their businesses so what is taxed is net profit. Businesses can also deduct the costs of purchases of machinery, software, buildings and so forth, but since these capital investments don’t lose value right away, these deductions are taken over time. In other words, capital expenses (expenditures to acquire or upgrade assets that generate income over a long period of time) usually must be written off over a number of years to reflect their ongoing usefulness.

In most cases firms would rather deduct capital expenses right away rather than delay these deductions because of the time value of money ( e.g. a given amount of money is worth more today than the same amount of money will be worth if it is received later.) For example, $100 invested now at a 7 percent return will grow to $200 in ten years.

A report from the Congressional Research Service reviews efforts to quantify the impact of bonus depreciation and explains that “the studies concluded that accelerated depreciation in general is a relatively ineffective tool for stimulating the economy.”[1]

Research Tax Credit

10 Year Cost: $109 billion

Rather than just extending the research credit, the House has passed legislation nearly doubling the cost of the tax credit.[2] Given the myriad problems with the research credit, Congress would be better off substantially reforming the credit or letting it expire entirely but should not expand the credit.[3]

One aspect of the credit that needs to be reformed is the definition of “research.” As it stands now, accounting firms are helping companies obtain the credit to subsidize redesigning food packaging and other activities that most Americans would see no reason to subsidize. The uncertainty about what qualifies as eligible research also results in substantial litigation and seems to encourage companies to push the boundaries of the law.

Another aspect of the credit that needs to be reformed is the rule governing how and when firms obtain the credit. For example, Congress should bar taxpayers from claiming the credit on amended returns because it is absurd to infer that the credit retroactively encouraged research.

As it stands now, some major accounting firms approach businesses and tell them that they can identify activities the companies carried out in the past that qualify for the research credit, and then help the companies claim the credit on amended tax returns. When used this way, the credit does not accomplish the goal of increasing the amount of research conducted by businesses.

The Offshore Loopholes

Active Financing Exception (aka GE Loophole)

10 Year Cost: $78 Billion

“Subpart F” of the tax code attempts to bar American corporations from “deferring” (delaying) paying U.S. taxes on certain types of offshore profits that are easily shifted out of the United States, such as interest income. The “active financing” exception to subpart F allows American financial corporations to defer paying taxes on offshore income even though such income is often really earned in the U.S. or other developed countries, but has been artificially shifted into an offshore tax haven to avoid taxes.

The “active financing” exception should have never been a part of the tax code.

The U.S. technically taxes the worldwide corporate profits, but American corporations can “defer” (delay indefinitely) paying U.S. taxes on “active” profits of their offshore subsidiaries until those profits are officially brought to the U.S. “Active” profits are what most ordinary people would think of as profits earned directly from providing goods or services.

“Passive” profits, in contrast, include dividends, rents, royalties, interest and other types of income that are easier to shift from one subsidiary to another. Subpart F tries to bar deferral of taxes on such kinds of offshore income. The so-called “active financing exception” makes an exception to this rule for profits generated by offshore financial subsidiaries doing business with offshore customers.

The active financing exception was repealed in the loophole-closing1986 Tax Reform Act, but was reinstated in 1997 as a “temporary” measure after fierce lobbying by multinational corporations. President Clinton tried to eliminate the provision with a line-item veto; however, the Supreme Court ruled the line-item veto unconstitutional and reinstated the exception. In 1998 Congress expanded the provision to include foreign captive insurance subsidiaries. It has been extended numerous times since 1998, usually for only one or two years at a time, as part of the tax extenders.

As explained in another report from Citizens for Tax Justice, the active financing exception provides a tax advantage for expanding operations abroad. It also allows multinational corporations to avoid tax on their worldwide income by creating “captive” foreign financing and insurance subsidiaries.[4] The financial products of these subsidiaries, in addition to being highly fungible and highly mobile, are also highly susceptible to manipulation or “financial engineering,” allowing companies to manipulate their tax bill as well.

The exception is one of the reasons that General Electric paid, on average, only a 1.8 percent effective U.S. federal income tax rate over 10 years. G.E.’s dramatically lowered its federal tax bill by using the active financing exception provision by its subsidiary, which Forbes noted has an “uncanny ability to lose lots of money in the U.S. and make lots of money overseas.”[5]

Controlled Foreign Corporations Look-Through Rule (aka Apple Loophole)

10 Year Cost: $21.8 billion

The “CFC look-thru rule” allows U.S. multinational corporations to create “nowhere income,” or profits that are not taxed by any country. It allows U.S. parent companies to treat foreign subsidiaries as corporations in one country but as non-existent in another country (typically the U.S.) The result is that the subsidiary generates deductible payments in one country, but reports no corresponding taxable income in a second, low- or no-tax country.

The closely watched 2013 Apple investigation by the Senate Permanent Subcommittee on Investigations resulted in a memorandum — signed by the subcommittee’s chairman and ranking member, Sens. Carl Levin and John McCain — that listed the CFC look-through rule as one of the loopholes used by Apple to shift profits abroad and avoid U.S. taxes.[6]

Section 179 Small Business Expensing

10 Year: $68.8 billion

Congress has showered businesses with several types of depreciation breaks, that is, breaks allowing firms to deduct the cost of acquiring or developing a capital asset more quickly than the asset actually wears out. Section 179 allows smaller businesses to write off most of their capital investments immediately (up to certain limits). A report from the Congressional Research Service reviews efforts to quantify the impact of depreciation breaks and explains that “the studies concluded that accelerated depreciation in general is a relatively ineffective tool for stimulating the economy.”[7]

Section 179 allows firms to deduct the entire cost of equipment purchases (to “expense” them) up to a limit. The most recent tax extenders package included provisions that allowed expensing of up to $500,000 of equipment purchases. The deduction is phased out when such purchases exceed $2 million.

Often, the actual beneficiaries of this provision are not necessarily what people think of as “small businesses.” Still, there is little reason to believe that business owners, big or small, respond to anything other than demand for their products and services.

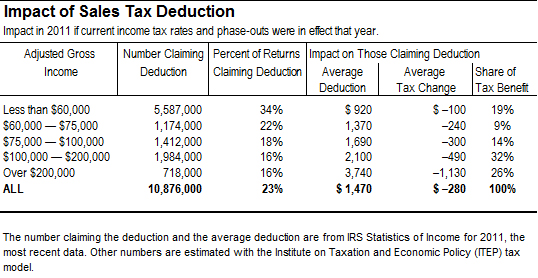

Deduction for State and Local Sales Taxes

10 Year: $42.4 billion

Permanent provisions in the federal personal income tax allow taxpayers to claim itemized deductions for property taxes and income taxes paid to state and local governments. Long ago, a deduction was allowed for state and local sales taxes, but that was repealed as part of the 1986 tax reform. In 2004, the deduction for sales taxes was brought back temporarily and extended several times since then.

Because the deduction for state and local sales taxes cannot be taken along with the deduction for state and local income taxes, in most cases, taxpayers will take the sales tax deduction only if they live in one of the handful of states that have no state income tax.

Taxpayers can keep their receipts to substantiate the amount of sales taxes paid throughout the year, but in practice most people use rough calculations provided by the IRS for their state and income level. People who make a large purchase, such as a vehicle or boat, can add the tax on such purchases to the IRS calculated amount.

There are currently nine states that have no broad-based personal income tax and rely more on sales taxes to fund public services. Politicians from these states argue that it’s unfair for the federal government to allow a deduction for state income taxes, but not for sales taxes. But this misses the larger point. Sales taxes are inherently regressive and allowing wealthy individuals to deduct these taxes helps perpetuate that inequality.

To be sure, lower-income people pay a much higher percentage of their incomes in sales taxes than the wealthy. But lower-income people also are unlikely to itemize deductions and are thus less likely to enjoy this tax break. In fact, the higher your income, the more the deduction is worth, since the amount of tax savings depends on your tax bracket.

The table above includes taxpayer data from the IRS for 2011 along with data generated from the Institute on Taxation and Economic Policy (ITEP) tax model to determine how different income groups would be affected by the deduction for sales taxes in the context of the federal income tax laws in effect today.

As illustrated in the table, people earning less than $60,000 a year who take the sales-tax deduction receive an average tax break of just $100, and receive less than a fifth of the total tax benefit. Those with incomes between $100,000 and $200,000 enjoy a break of almost $500 and receive a third of the deduction, while those with incomes exceeding $200,000 save $1,130 and receive just over a fourth of the total tax benefit.

Work Opportunity Tax Credit

10 Year: $17.4 billion

The Work Opportunity Tax Credit ostensibly helps businesses hire welfare recipients and other disadvantaged individuals. But a report from the Center for Law and Social Policy concludes that it mainly provides a tax break to businesses for hiring they would have done anyway:[8]

WOTC is not designed to promote net job creation, and there is no evidence that it does so. The program is designed to encourage employers to increase hiring of members of certain disadvantaged groups, but studies have found that it has little effect on hiring choices or retention; it may have modest positive effects on the earnings of qualifying workers at participating firms. Most of the benefit of the credit appears to go to large firms in high turnover, low-wage industries, many of whom use intermediaries to identify eligible workers and complete required paperwork. These findings suggest very high levels of windfall costs, in which employers receive the tax credit for hiring workers whom they would have hired in the absence of the credit.

15-Year Cost Recovery Break for Leasehold, Restaurants, and Retail

10 Year: $17 billion

Congress has showered all sorts of businesses with breaks that allow them to deduct the cost of developing capital assets more quickly than they actually wear out. This particular tax extender allows certain businesses to write off the cost of improvements made to restaurants and stores over 15 years rather than the 39 years that would normally be required.

It is unclear why helping restaurant owners and store owners improve their properties should be seen as more important than nutrition and education for low-income children or unemployment assistance or any of the other benefits that lawmakers insist cannot be enacted if they increase the deficit.

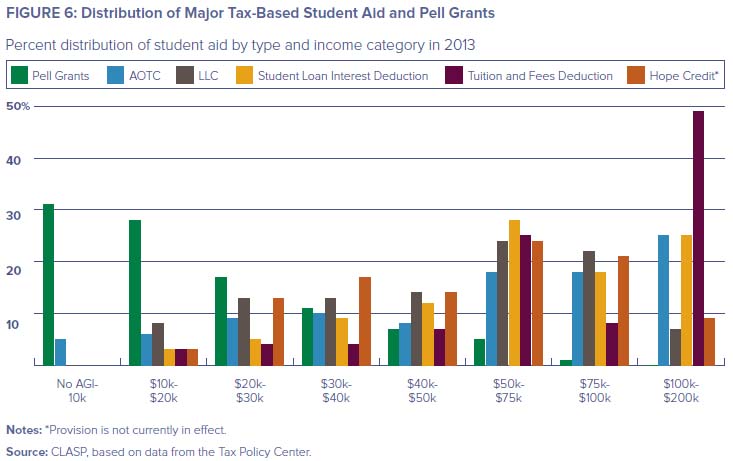

Deduction for Tuition and Related Expenses

10 Year: $5.1 billion

The limited deduction for tuition and related expenses is not among the larger tax extenders, but it’s worth understanding because it is one of the provisions that lawmakers sometimes cite as a reason to support the tax extenders legislation. This deduction makes up only 0.7 percent of the cost of the entire tax extenders legislation. It is not justification for passing this costly legislation.

The deduction for tuition and related expenses is the most regressive tax break for postsecondary education. The distribution of tax breaks for postsecondary education among income groups is important because if their purpose is to encourage people to obtain education, they will be more effective if they are targeted to lower-income households that could not otherwise afford college rather than well-off families that will send their kids to college no matter what.

The graph below compares the distribution of various tax breaks for postsecondary education as well as Pell Grants.

The graph illustrates that not all tax breaks for postsecondary education are the same, and the deduction for tuition and related expenses is the most regressive of the bunch. Some of these tax breaks are more targeted to those who really need them, although none are nearly as well-targeted to low-income households as Pell Grants. Tax cuts for higher education taken together are not well-targeted, as illustrated in the bar graph below. Americans paying for undergraduate education for themselves or their kids in 2009 or later generally have no reason to use the deduction because starting that year another break for postsecondary education was expanded and became more advantageous.

[1] Gary Guenther, Section 179 and Bonus Depreciation Expensing Allowances: Current Law, Legislative Proposals in the 112th Congress, and Economic Effects, September 10, 2012. http://www.fas.org/sgp/crs/misc/RL31852.pdf

[2] Citizens for Tax Justice, “House Leadership Content to Balloon the Deficit for the Sake of Corporate Tax Breaks,” May 20, 2015. http://www.taxjusticeblog.org/archive/2015/05/house_leadership_content_to_ba.php

[3] Citizens for Tax Justice, “Reform the Research Credit — Or Let It Die,” December 4, 2013. http://ctj.org/ctjreports/2013/12/reform_the_research_tax_credit_–_or_let_it_die.php

[4] Citizens for Tax Justice, “Don’t Renew the Offshore Tax Loopholes,” August 2, 2012. www.ctj.org/ctjreports/2012/08/dont_renew_the_offshore_tax_loopholes.php

[5] Christopher Helman, “What the Top U.S. Companies Pay in Taxes,” Forbes, April 1, 2010, http://www.forbes.com/2010/04/01/ge-exxon-walmart-business-washington-corporate-taxes.html.

[6] Senators Carl Levin and John McCain, Memorandum to Members of the Permanent Subcommittee on Investigations, May 21, 2013. http://www.hsgac.senate.gov/download/?id=CDE3652B-DA4E-4EE1-B841-AEAD48177DC4

[7] Gary Guenther, “Section 179 and Bonus Depreciation Expensing Allowances: Current Law, Legislative Proposals in the 112th Congress, and Economic Effects,” Congressional Research Service, September 10, 2012. http://www.fas.org/sgp/crs/misc/RL31852.pdf

[8] Elizabeth Lower-Basch, “Rethinking Work Opportunity: From Tax Credits to Subsidized Job Placements,” Center for Law and Social Policy, November 2011. http://www.clasp.org/resources-and-publications/files/Big-Ideas-for-Job-Creation-Rethinking-Work-Opportunity.pdf

Want even more CTJ? Check us out on Twitter, Facebook, RSS, and Youtube!